Cintas NASDAQ: CTAS the share price isn’t low, trading at 37x current year earnings, about 65% more expensive than the average S&P 500 company, but this is about as cheap as it’s going to get.

While operational concerns have moderated the share price, fears about Unifirst NYSE: UNF Acquisitions, regulatory scrutiny, and energy cost storms have failed to derail the business. Cintas is a leading player in uniformed services, doing well in fiscal year 2026 and is on track to strengthen in 2027.

Unifirst can be both a hindrance and a catalyst this year. UNF shareholders approved the merger, but the Federal Trade Commission did not.

On the one hand, the merger will allow for many of the proven synergies that Cintas has opened up through past acquisitions, while expanding its footprint and cross-selling opportunities – suitable for growth and margin. On the other hand, a blocked deal would mean that Cintas could continue to push as it is, outpace competitors, increase market share, drive more revenue, and return money to its investors—good for its share price.

Cintas Advances After Beat-and-Raise Quarter

Cintas reported another good quarter on July 15, with revenue and profit exceeding expectations despite the impact of acquisition-related costs. Revenue grew 9% to $2.91 billion, beating consensus by nearly 140 basis points. Power is supported by the core Similar Services segment, which grew by 8.2%, and is driven by the Other segment, which grew by over 11%. The other segment includes security, fire, and first aid, all of which cross-sell with supermarkets.

Margin news was also positive. The company expanded its gross and operating margins, increasing its gross margin by 11.6% and its operating ratio by 12.7%, leaving earnings to rise at more than double the pace of revenue growth. Adjusted earnings per share (EPS) rose 18.3%, besting 5 cents, including the 3-cent impact of acquisition costs. More importantly, full-year cash flow came in at $2.28 billion, up 5% year-over-year (YOY) and sufficient to cover capital expenditures and acquisition costs while paying a dividend.

The highlights of Cintas’ financial year-end balance sheet showed the strength of the model and its location. Current and net assets were increased by cash, receivables, and assets, while long-term debt and liabilities were declined, dividends were paid, and shares were repurchased. The result was an increase in equity of 9.7% and a reduction in share price of 1% YOY, with a profit margin of about 1%. The assumption is that CTAS shares have paid 1%, while investors have received 1% in equity and about 10% in equity, metrics that support share price growth over time.

Analysts and Institutions Show Confidence in CTAS’s Long-Term Strength

Cintas’ Q4 results and guidance update may not inspire a strong round of analyst reviews, but should be enough to offset the price’s decline. The downtrend helped lower stock prices and masked a bullish market.

The current analyst consensus is Hold, which is not surprising given the execution risks involved in the Unifirst merger, and the price target suggests a slight upside to the recent lows. Chances are that analyst sentiment will cease to hold in future positions, triggering more bullish activity in the market.

Institutions, on the other hand, are more active than analytical styles. The group owns 63% of the stock and has been buying heavily for the last 12 months. Activity was reduced before the release but showed a strong market, increasing at a pace of $4 to $1. The likely outcome is that, given the low price and technical setup, institutions will continue to accumulate CTAS shares and limit potential risks.

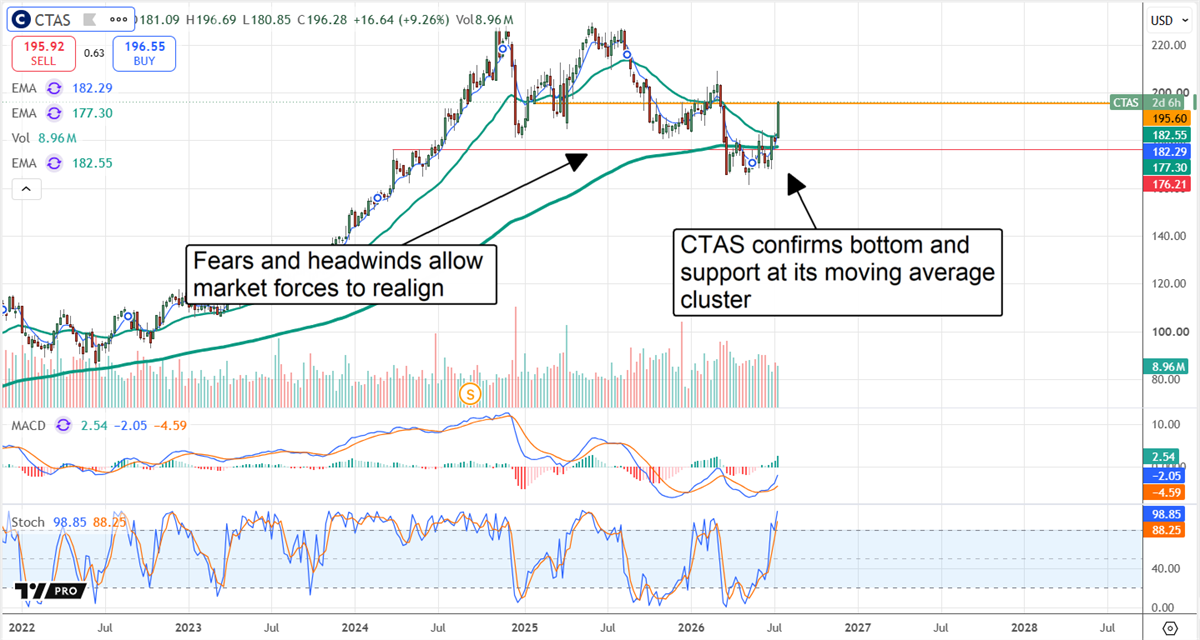

Charts suggest that CTAS has bottomed out over the past year and is in recovery mode from mid-2026. Price action moved above key support before the release and accelerated after, showing support in a set of exponential moving averages (EMAs), including both long-term and short-term indicators. Market forces are well aligned, and the price is set to support a rally in the coming quarters. In this scenario, the CTAS is on track to retest its current highs within the next 12 months and is likely to continue higher thereafter.

Basically, Cintas is well placed to benefit from the economic results. This year’s labor market data is not strong but shows growth and stability, including improvements in overall jobless claims that point to similar demand and demand for services. With labor markets supported by business investment, deregulation, and favorable tax policies (as JPMorgan CEO Jamie Dimon recently pointed out), Cintas’ business will remain healthy for the foreseeable future and may even accelerate.

Before you consider Cintas, you’ll want to hear this.

MarketBeat tracks Wall Street’s top and most effective research analysts and the stocks they recommend to their clients every day. MarketBeat identified five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on… and Cintas wasn’t on the list.

Although Cintas currently has an Average Buy rating among analysts, top analysts believe these five stocks are the best.

View Five Stocks Here

MarketBeat recently released its list of the 7 hottest IPOs expected to hit Wall Street in 2026. See which companies are preparing to go public and why investors are watching closely.

Get This Free Report